You already know health insurance can be expensive, and finding something affordable often feels confusing. What many people miss is that the cheapest monthly premium is not always the cheapest plan overall. In this guide, you’ll learn how to compare affordable options, lower your costs, and choose coverage that actually protects you.

Key Takeaways

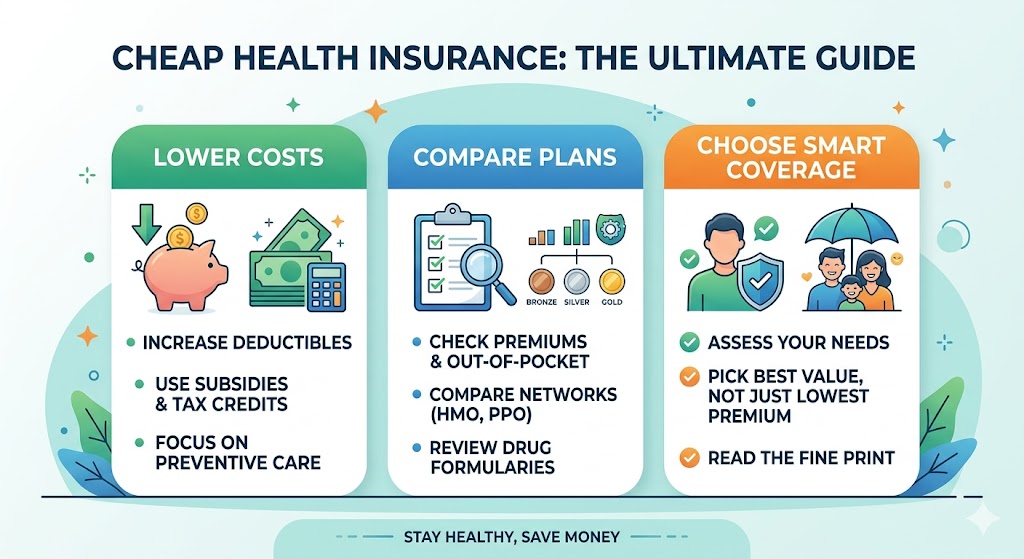

- Cheap health insurance means low total cost, not just the lowest monthly premium. Premiums, deductibles, and out-of-pocket costs must be reviewed together.

- Affordable coverage can come from multiple sources, including ACA Marketplace plans, Medicaid, employer plans, student plans, and catastrophic coverage.

- ACA subsidies can lower premiums significantly for eligible households based on income and family size.

- Provider networks matter because out-of-network care can become expensive fast. Always check doctors, hospitals, and prescriptions before enrolling.

- Annual comparison saves money. Plans, subsidies, and your health needs can change every year.

- A simple checklist prevents common mistakes. Comparing total yearly cost is safer than choosing by price alone.

- Affordable coverage is possible for freelancers, families, and individuals when you compare options strategically.

What Is Cheap Health Insurance and How Does It Work?

Cheap health insurance is coverage with the lowest reasonable total annual cost based on premiums, deductibles, and expected medical use. In simple terms, a plan is “cheap” when it fits your budget while still protecting you from large medical bills.

First, many people focus only on the monthly premium. That is the amount you pay every month to keep coverage active. However, a low premium can hide a high deductible or costly copays.

For example, Plan A may cost $150 monthly with a $7,000 deductible, while Plan B may cost $250 monthly with a $1,500 deductible. If you need regular care, Plan B could cost less overall.

Health insurance premiums are the monthly amount paid to keep coverage active, regardless of whether care is used.

In addition, cheap medical insurance often depends on your income, age, family size, location, and whether you qualify for assistance programs. That is why two people may see very different prices for the same insurer.

how health insurance deductibles work

Why Cheap Health Insurance Matters

Cheap health insurance matters because affordable coverage reduces financial risk, improves access to care, and creates peace of mind. Without insurance, even one emergency can create major debt.

First, emergency room visits can cost thousands of dollars. A hospital stay can cost far more. Medical debt remains a major financial burden for many households — Source: KFF, 2025.

Second, preventive care can help catch problems early. Many plans cover screenings, vaccines, and annual checkups at low or no cost when in-network. That can reduce long-term expenses.

For example, managing high blood pressure early may prevent expensive complications later. This is why affordable insurance is about protection, not only price.

Third, coverage helps with prescriptions and specialist visits. If you need asthma medication or diabetes supplies, insurance can dramatically reduce recurring costs.

preventive care covered by insurance

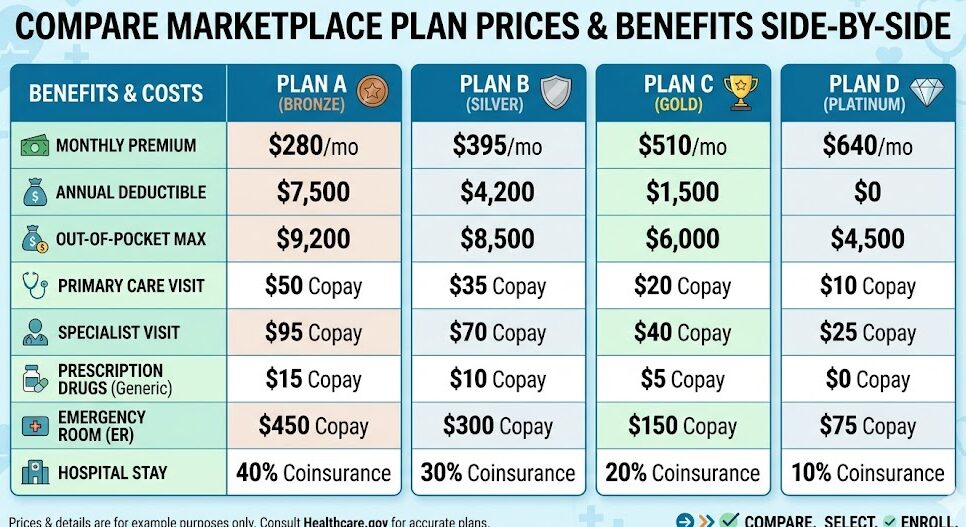

Why Is the Lowest Premium Not Always the Cheapest Plan?

The lowest premium is not always the cheapest plan because total healthcare cost includes deductibles, copays, coinsurance, and out-of-pocket maximums. A low monthly bill can lead to higher costs later.

Understanding the Main Costs

| Cost Type | What It Means | Why It Matters |

|---|---|---|

| Premium | Monthly payment | Paid whether you use care or not |

| Deductible | Amount you pay before many services start sharing costs | High deductibles increase early-year costs |

| Copay | Fixed fee per visit or prescription | Adds up with frequent care |

| Coinsurance | Percentage of bill after deductible | Expensive procedures can cost more |

| Out-of-Pocket Maximum | Most you pay in a year for covered care | Key protection limit |

First, a high-deductible plan may work well if you rarely use care. However, if you need tests, therapy, or prescriptions, total spending can rise quickly.

For example, a person who sees specialists monthly may save more with a higher premium but lower deductible plan.

A low-premium plan can cost more overall if it has a high deductible and high out-of-pocket expenses.

What Are the Cheapest Types of Health Insurance Plans Available?

The cheapest types of health insurance plans depend on eligibility, income, and life stage. Some options offer very low premiums, while others balance cost and benefits.

ACA Marketplace Plans

ACA health insurance is regulated individual coverage sold through the Marketplace with essential benefits and subsidy eligibility. Many users find affordable health insurance here.

Moreover, 4 out of 5 Marketplace consumers can find plans for $10 or less per month after subsidies in many cases — Source: CMS, 2025.

ACA subsidy income limits guide

Medicaid

Medicaid is government health coverage for eligible low-income individuals and families. For qualifying users, it may be the best low-cost option.

Benefits and eligibility vary by state, so always verify current rules.

Employer-Sponsored Plans

Employer coverage is insurance offered through a workplace, often with employer contributions. This can reduce monthly premiums significantly.

For example, employers often pay part of the premium, making coverage cheaper than buying alone.

Catastrophic Plans

Catastrophic health insurance is a low-premium plan designed mainly for worst-case events. It usually has high deductibles and is often available to younger users or hardship exemptions.

Student Plans and Community Programs

Student health plans are campus-based insurance options for enrolled students. In some cases, local clinics or community programs also provide affordable services.

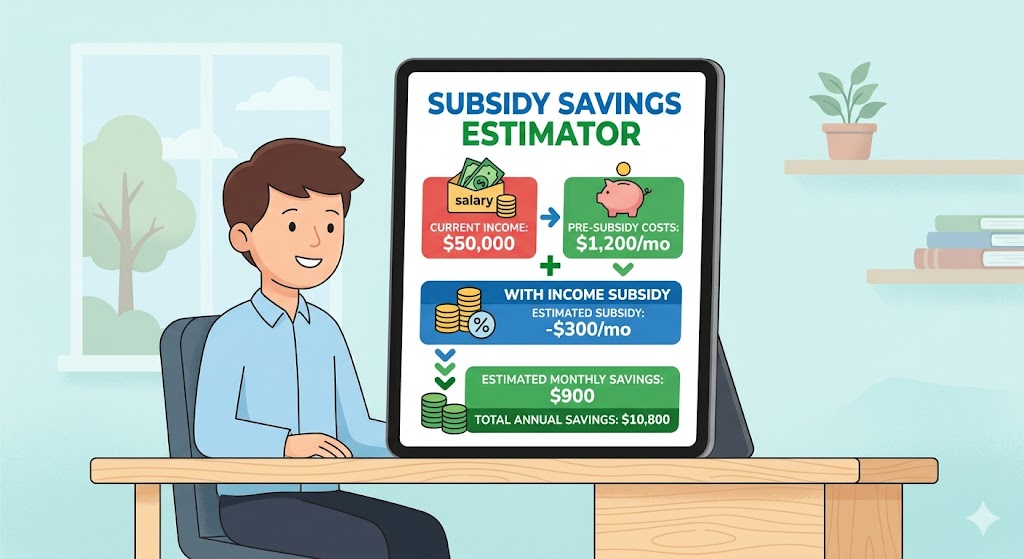

How Do ACA Subsidies Lower Health Insurance Costs?

ACA subsidies lower health insurance costs by reducing monthly premiums and, in some cases, lowering out-of-pocket expenses for eligible households. These savings depend on income and household size.

First, premium tax credits lower what you pay each month. Second, cost-sharing reductions may reduce deductibles and copays for some enrollees on eligible plans.

For example, a self-employed person earning moderate income may qualify for a much lower premium than the listed sticker price.

ACA subsidies reduce eligible users’ monthly Marketplace premiums based on household income and family size.

That being said, income changes during the year can affect final subsidy amounts. Report life changes promptly.

ways to lower monthly insurance premiums

How Can Self-Employed Workers Get Cheap Health Insurance?

Self-employed workers can get cheap health insurance through ACA Marketplace plans, subsidies, professional associations, spouse plans, or Medicaid if eligible. Freelancers often need flexible solutions.

Best First Step: Check Marketplace Savings

First, estimate annual income carefully. This helps determine subsidy eligibility and avoids surprises later.

For example, a freelancer with fluctuating income may still qualify for meaningful assistance based on projected earnings.

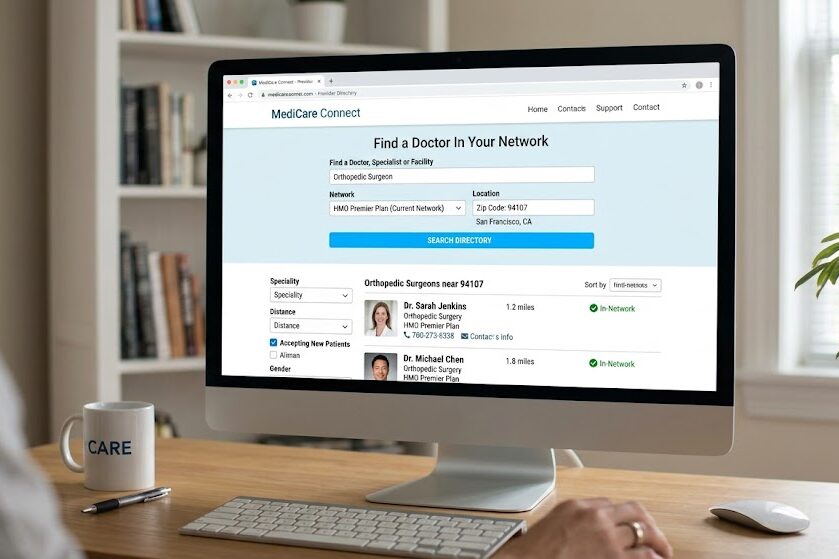

Compare Networks and Prescriptions

Second, compare doctors, hospitals, and medications before enrolling. The wrong network can increase costs fast.

Comparing provider networks, prescriptions, and total yearly cost is the safest way to choose affordable health insurance.

best health insurance for freelancers

prescription drug coverage checklist

How Do You Compare Cheap Health Insurance Plans Step by Step?

Comparing cheap health insurance plans step by step means reviewing total cost, coverage fit, provider access, and eligibility before enrolling. A simple framework makes decisions easier.

Step 1: Estimate Your Healthcare Use

First, think about likely care needs this year.

- Rare doctor visits

- Ongoing prescriptions

- Planned surgery

- Therapy or specialist care

- Family pediatric visits

For example, frequent care usually favors lower deductibles.

Step 2: Compare Total Annual Cost

Second, add likely premium cost plus expected medical spending.

Formula:

Annual Premiums + Expected Out-of-Pocket Costs = Estimated Total Cost

Step 3: Check Networks

Third, confirm your preferred doctors and hospitals are in-network.

Step 4: Review Drug Coverage

Fourth, search your medications on each plan formulary.

Step 5: Check Maximum Protection

Finally, compare the out-of-pocket maximum. Lower limits can protect you in bad years.

how to compare health insurance plans

What Mistakes Should You Avoid When Buying Cheap Health Insurance?

The biggest mistakes when buying cheap health insurance are choosing by premium only, ignoring deductibles, missing deadlines, and skipping network checks. Small mistakes can become expensive.

First, many buyers ignore the deductible. A $0 doctor visit benefit may not apply to everything.

Second, some users forget enrollment windows. Missing deadlines can delay coverage.

Third, others assume every doctor accepts every plan. Always verify first.

Fourth, some shoppers underestimate family needs. Children, maternity care, or specialist visits can change the best option.

For example, a family may save with a slightly higher premium plan that has lower pediatric costs.

family health insurance cost guide

open enrollment deadlines explained

Tools and Practical Applications to Find Affordable Health Insurance

The best tools for finding cheap health insurance help you compare plans, estimate subsidies, and review provider access before enrollment. Free tools can simplify the process.

Useful Tools

- Health Insurance Marketplace – Compare ACA plans and subsidy estimates.

- State Medicaid Portals – Check local eligibility.

- Insurer Provider Directories – Confirm doctors and hospitals.

- Prescription Lookup Tools – Review covered medications.

- Budget Spreadsheet or Calculator – Estimate annual cost.

Practical Example

Single adult, healthy, few visits: low premium may work.

Family with children and prescriptions: lower deductible may win.

Freelancer with uncertain income: subsidy estimate is essential.

What’s Next: How to Enroll and Keep Costs Low

The next step after comparing cheap health insurance is to gather documents, enroll on time, and review your plan every year. Action beats delay.

- Gather income documents and household details.

- List doctors and prescriptions.

- Compare at least three plans.

- Check subsidy or Medicaid eligibility.

- Enroll before deadlines.

- Review again next year or after life changes.

Moreover, life changes such as marriage, job loss, moving, or having a baby may unlock special enrollment rights.

when to change health insurance plans

Conclusion

Cheap health insurance is possible when you compare total value instead of chasing the lowest sticker price. The smartest plan balances affordable premiums, manageable deductibles, strong provider access, and real financial protection.

By reviewing subsidies, Medicaid eligibility, yearly costs, and your care needs, you can choose coverage confidently. Start comparing today, because the best affordable plan is the one that protects both your health and your budget.

Written by: Suraj — 5+ Blogger, SEO content writer specializing in high-ranking educational guides, comparison content, and AI-optimized publishing strategies.

Reviewed by: Editorial Health Content Team — Research reviewers focused on consumer health insurance literacy, policy clarity, and fact-checking.

Disclaimer: This article was initially drafted using AI assistance. However, the content has undergone thorough revisions, editing, and fact-checking by human editors and subject matter experts to ensure accuracy.